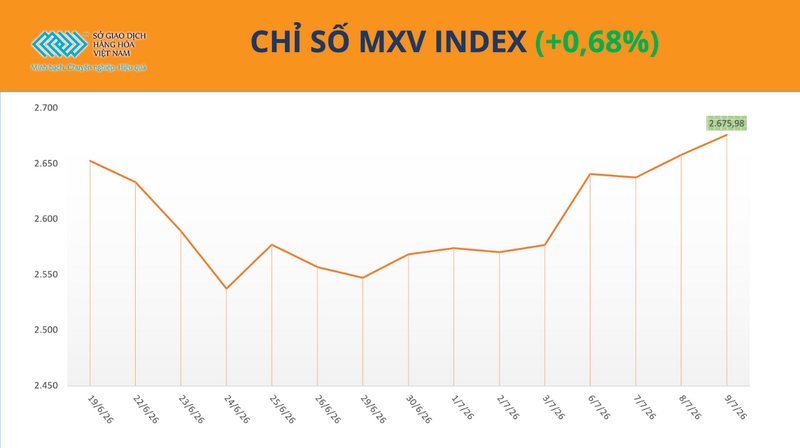

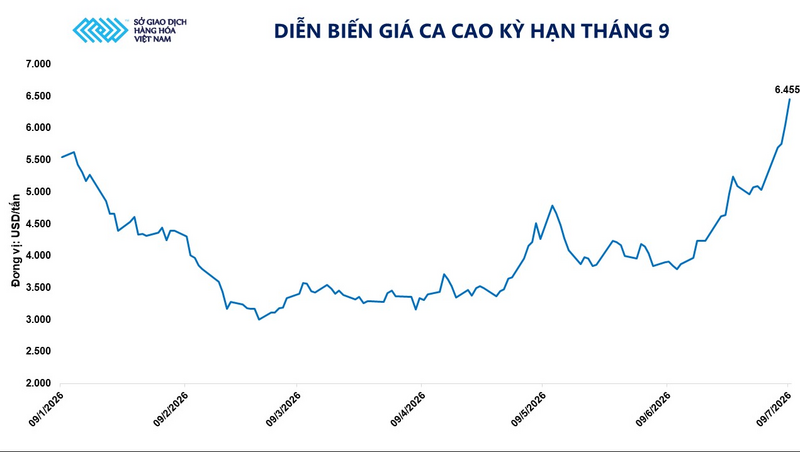

Buying pressure dominated the global commodities market on July 9th, supporting the MXV-Index's third consecutive day of gains, reaching 2,675 points. The focus remained on industrial raw materials, with cocoa prices surging 6.66% to near $6,500 per ton – the highest level since April 2025.

MXV-Index

Adverse weather conditions in West Africa continue to drive up cocoa prices.

According to data from the Vietnam Commodity Exchange, at the close of yesterday's trading session, September cocoa futures rose 6.66% to $6,455 per ton, marking the fourth consecutive day of gains. The main driving force came from the market's continued raising of its assessment of supply shortage risks in the 2026-2027 crop year, following less optimistic production prospects in Ivory Coast – the world's largest cocoa producer.

Cocoa futures price chart for September delivery. Source: MXV

This concern stems from the prolonged extreme weather events in West Africa, particularly in Ivory Coast and Ghana. Field surveys indicate that the region is experiencing unusual weather patterns, amid fears of a potentially strong super El Niño in about 75 years forming over the Pacific Ocean. Since March, temperatures in both countries have been approximately 1.1°C lower than the five-year average, while rainfall in June surged, exceeding multi-year averages by 46% in Ivory Coast and 52% in Ghana, respectively.

Prolonged heavy rainfall has not only flooded many plantations, disrupting harvesting and transportation, but has also increased humidity, creating favorable conditions for fungal diseases, especially black rot, to thrive during the fruiting and ripening stages. This raises concerns about the yield of the new crop. Some analytical organizations currently forecast Ivory Coast's cocoa production in the 2026-2027 crop year to reach only about 1.7-1.8 million tons, a decrease of about 18% compared to the 2.2 million tons of the previous crop year.

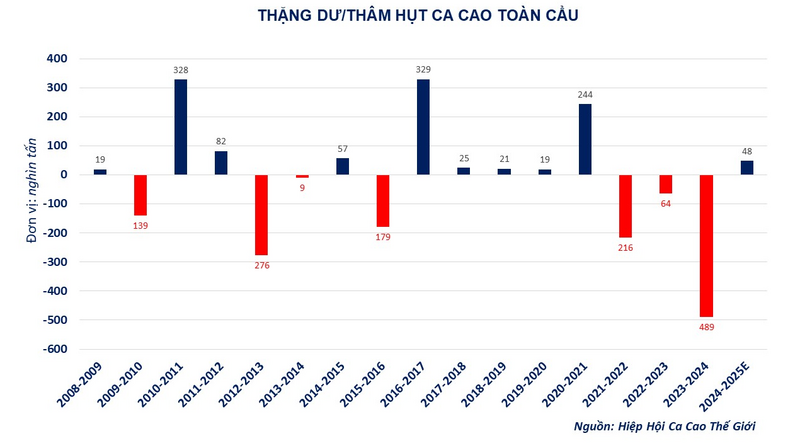

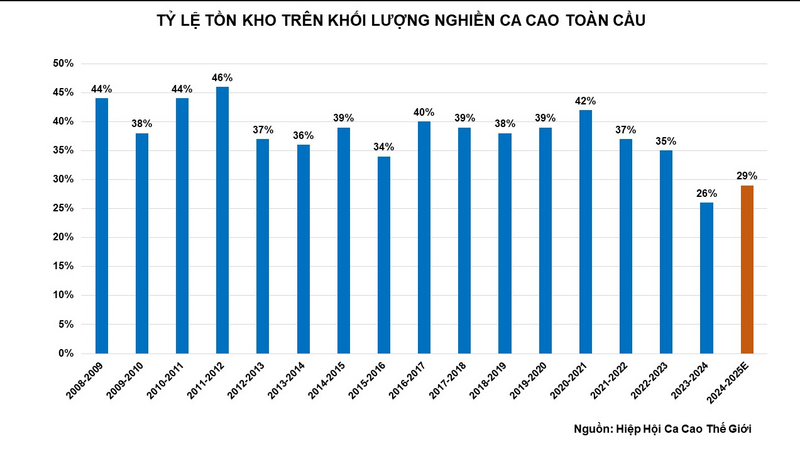

From a long-term perspective, the global supply and demand picture has not really improved. According to the International Cocoa Organization (ICCO) report in May 2026, the forecast for the global cocoa surplus in the 2024-2025 crop year has been revised down to 48,000 tonnes, significantly lower than the previously projected 75,000 tonnes. Although the stock-to-grinding ratio has recovered from its low point in the 2023-2024 crop year, it remains below historical averages, indicating that the supply available on the market is not yet abundant.

Global cocoa surplus/deficit. Source: MXV

Global cocoa inventory-to-ground volume ratio

In addition, the market continues to closely monitor the risk of El Niño strengthening in the second half of the year. If this phenomenon develops in an unfavorable direction, hot and dry Harmattan winds could appear in West Africa, reducing soil moisture, increasing stress on crops, and affecting yield prospects for the next season.

Conversely, the upward trend in cocoa prices has been somewhat restrained due to the relatively strong availability of spot supply. As of June 28th, cocoa arrivals at Ivory Coast ports since the beginning of the crop year (October 1st) reached 1.91 million tons, an 18.4% increase compared to the same period last year. Alongside this, Nigeria's cocoa exports in May also increased by over 28% year-on-year, reaching over 18,000 tons. However, these figures only reflect the supply of the current crop year, while capital flows in the futures market are focusing more on the production prospects of the new crop.

Wheat prices are rising ahead of the release of the WASDE report.

The global wheat market saw a positive trading session as speculative capital returned ahead of the US Department of Agriculture (USDA) release of its July World Agricultural Supply and Demand (WASDE) report. Expectations that the agency would revise down ending stocks in the US fueled buying in the futures market even before the report was released.

At the close of trading, Chicago wheat prices rose nearly 2% to $227 per ton, while Kansas wheat prices increased 1.4% to $240.4 per ton. The MXV-Index for agricultural products also closed at 1,437 points. Liquidity in the agricultural sector remained stable, reflecting continued positive capital inflow into the market and no signs of slowing demand from investors to balance their positions.

The main driver of the price surge came from portfolio positioning by speculators ahead of the WASDE report release. Analysts forecast that the USDA could cut approximately 816,470 tons of US wheat inventories for the 2026-2027 crop year, bringing ending stocks down to around 19.4 million tons.

On the production side, US winter wheat production is projected to decrease by approximately 789,249 tons compared to the June report. Although the improved outlook for spring wheat yields helps to reduce total production by only about 489,879 tons, to 41.5 million tons, the market remains cautious as medium- and long-term supply has not yet significantly improved.

This was further reinforced by the USDA's late-June planting acreage report. According to the report, the US spring wheat acreage fell to 3.8 million hectares – the lowest level in 56 years – while the winter wheat acreage decreased by approximately 360,170 hectares, to 12.76 million hectares. These figures further strengthen expectations that the US wheat supply in the new crop year will not be as abundant as in previous years.

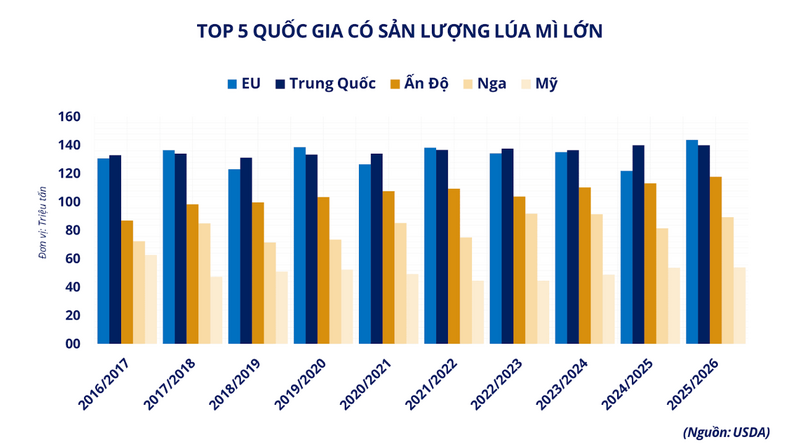

Top 5 countries with the largest wheat production. Source: MXV

Not only is the market affected by the supply outlook in the US, but it is also closely monitoring crop developments in many major wheat-producing and exporting countries around the world. In Australia, the risk of a Super El Niño phenomenon has led the country's meteorological agency to warn of a 60-80% probability of below-average rainfall in key wheat-growing regions in the coming months. If this scenario occurs, Australia's wheat production could fall by about 26%, to 26.7 million tons, while export volume is expected to decrease by about 10 million tons, equivalent to about 5% of global wheat trade. Meanwhile, the European Commission (EC) has also lowered its forecast for the EU's 2026-2027 soft wheat production to 126.3 million tons due to prolonged heatwaves and droughts in many producing regions, especially France.

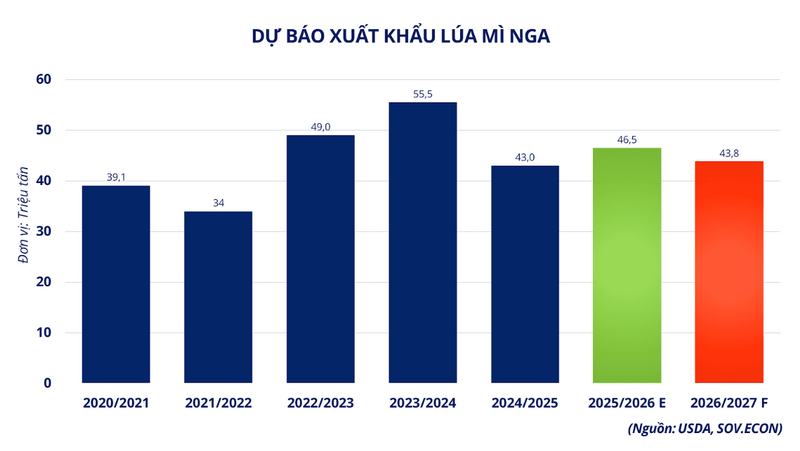

In the Black Sea region, difficulties in production and export continue to fuel concerns about global supply. In Russia, rainfall exceeding average by 60% to 118% in the Volga and Siberian regions has slowed spring wheat planting, resulting in a 12% decrease in planted area compared to the same period last year, to 7.1 million hectares. In addition, the impact of conflict has disrupted diesel supplies, increasing production costs. For Ukraine, escalating fertilizer costs and damage to the Odesa port system are raising concerns that monthly wheat exports could fall by as much as a third.

Forecast for Russian wheat exports. Source: MXV

In terms of demand, the market continues to receive support from the prospect of increased imports from China. Heavy rains and storms during the harvest season degraded the quality of approximately 7% of the country's total wheat production, forcing some to be diverted for animal feed. This has increased expectations that China will increase imports of high-quality wheat from the US and Western Europe in the second half of 2026, thereby further supporting wheat prices in the futures market.

Mr. Do Xuan Quy - Deputy General Director and Co-founder of 3D Commodity Trading Joint Stock Company, trading member No. 072 of MXV, said: " In the short term, wheat is in a rather sensitive phase to fundamental information, especially the WASDE report. After the report is released, the market is likely to experience strong fluctuations reflecting new data on global supply and demand."